Blog

Africa’s youth population is often described in extremes: a booming youth population and low employment shares. But the latest Africa Youth Employment Outlook 2026, produced by World Data Lab in partnership with the Mastercard Foundation and the University of Cape Town’s Development Policy Research Unit, tells a more nuanced, and more urgent, story.

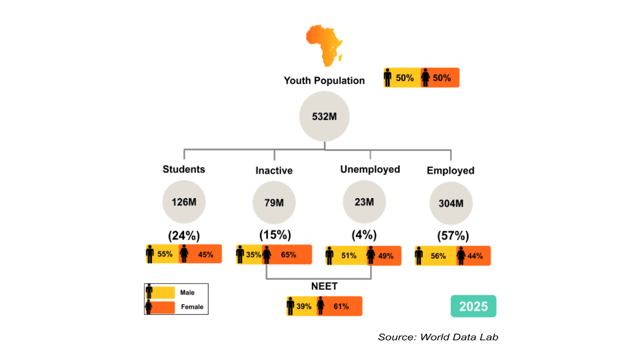

Contrary to conventional belief, young Africans work more than their peers on other continents. About 57% of youth in Africa, or 304 million, are estimated to be working as of 2025, compared with about 48% in the rest of the world. The challenge facing Africa’s youth is not just creating jobs, but also preventing the premature exit of school-age youth from school into low-paying informal agricultural work, strengthening employment stability and protections, and expanding pathways toward economic security.

Figure 1: Young Africans work more than their peers in the rest of the world

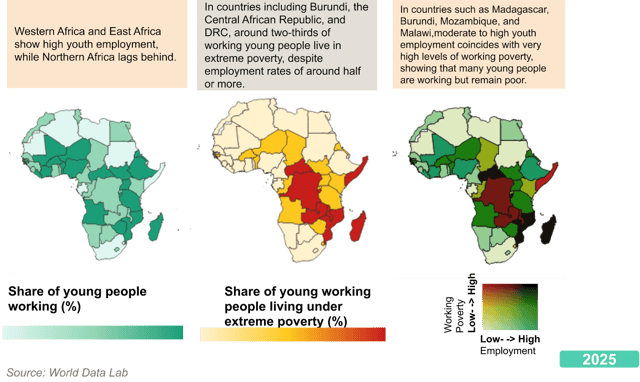

Insight 1: The jobs paradox - More work often coincides with higher poverty

Our data reveals a jobs paradox. High employment numbers conceal a harsh reality: working does not guarantee a pathway out of poverty. Countries with some of the highest youth employment shares, such as Madagascar (80%) and Tanzania (79%), also report high shares of working poverty. Across the continent, 104 million young workers, or 34%, live in households categorized as extremely poor. One key driver of this paradox is informality. A staggering 90% of employed young Africans work in informal jobs that lack contracts, social protection, and stability.

Figure 2: The Jobs Paradox - More work often coincides with higher poverty

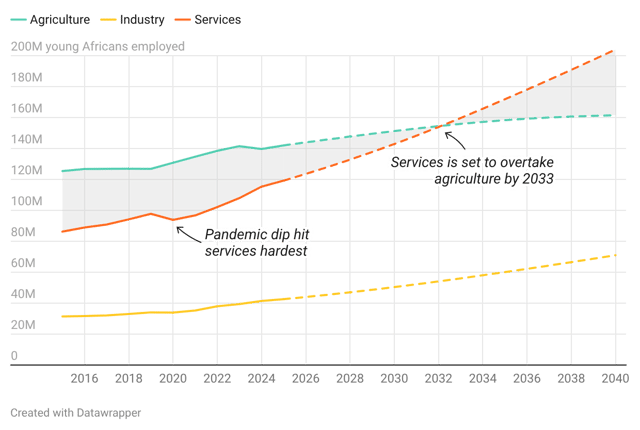

Insight 2: A historic shift from agriculture to services

We are currently witnessing a structural transformation in African economies. For decades, agriculture has been the dominant youth employer, but its grip is loosening. While agriculture currently employs 47% of young Africans, the services sector is expanding nearly twice as fast.

World Data Lab projects that by 2033, the services sector will overtake agriculture as the largest employer of young Africans.

Rather than following the traditional path from agriculture to manufacturing, which faces high energy and infrastructure costs, some African economies appear to be “leapfrogging” the industrial phase, with employment growth occurring directly in service sectors such as trade, transport, and digital work as urbanisation increases. While services generally offer higher wages, roughly 2.6 times more than agriculture in selected countries, the sector remains highly heterogeneous. Without policy intervention, many of these new service jobs may remain informal and low-productivity.

Figure 3: By 2033, services will become the largest employer of young Africans, overtaking the long-dominant agriculture sector

Insight 3: Higher growth does not automatically translate to high job creation.

Why isn't economic growth solving the employment challenge? The report identifies a critical disconnect between GDP growth and job creation, measured by employment elasticity.

Employment elasticity indicates how much employment changes in response to economic growth. For the period 2005–2023, the employment elasticity for African youth was just 0.44. This means that for every 1% of GDP growth, youth employment only grew by 0.44%.

This elasticity is significantly lower than the aggregate for the total population (0.50), indicating that economic growth yields weaker employment gains for young people than for older age groups. Furthermore, sectoral elasticities reveal a sharp divide: while industry (0.78) and services (0.76) are highly responsive to growth, agriculture (0.17) remains stagnant. To absorb the 10 million young people entering the labor market annually, African economies must not only grow, but grow in the right sectors.

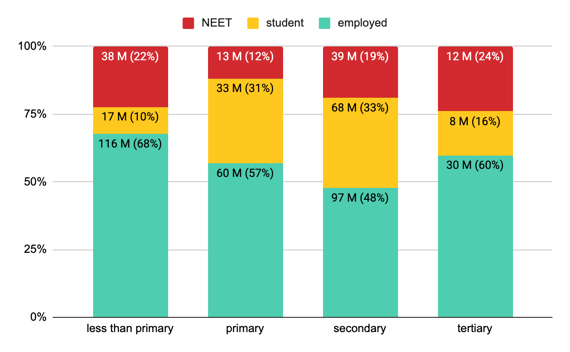

Insight 4: Education alone is not enough

As of 2025, only 9% of young Africans have completed tertiary education. While this limits access to high-skill jobs, the report finds that even among tertiary-educated youth, unemployment and inactivity remain high in several regions, particularly in North Africa. In economies such as Algeria, Egypt, and Morocco, nearly 30% of university graduates remain unemployed or inactive. This disconnect is driven by a private sector that is growing too slowly to absorb the rising supply of graduates, alongside a persistent mismatch and inadequacy in skills acquired in school compared with those required at work. Without better alignment between curricula and labor market needs, African nations risk expanding education systems that produce graduates without improving employment outcomes.

Figure 4: A higher share of young Africans with less than primary education is employed compared with those with higher education attainment

Insight 5: The gender gap: The hidden cost of care

The employment outlook is particularly stark for young women. Women make up nearly 61% (62 million) of all youth not in employment, education, or training (NEET).

This exclusion is rarely a choice. In Sub-Saharan Africa, 28% of women outside the labor force cite unpaid care responsibilities as the primary reason for their non-participation, compared to only 3% of men. Data shows that in countries like Egypt, women spend up to 9.2 times as much time on unpaid care work as men.

While young women are gaining a larger share of jobs in the agriculture sector, they remain underrepresented in the higher-growth industry and services sectors. Unlocking Africa’s full potential requires dismantling these barriers through policies that redistribute the care burden and keep young women in school longer.

Figure 5: Women make up about 61% of young people who are NEET

Africa’s demographic advantage can translate into shared prosperity if policy and investment choices focus on labour-absorbing growth, job quality, and inclusion. Evidence from across the continent points to four priorities.

Read the full Africa Youth Employment Outlook 2026 report for detailed country-level data and sector-specific forecasts.